What does a person's total financial standing truly reflect? Understanding the fundamental concept of a comprehensive financial assessment.

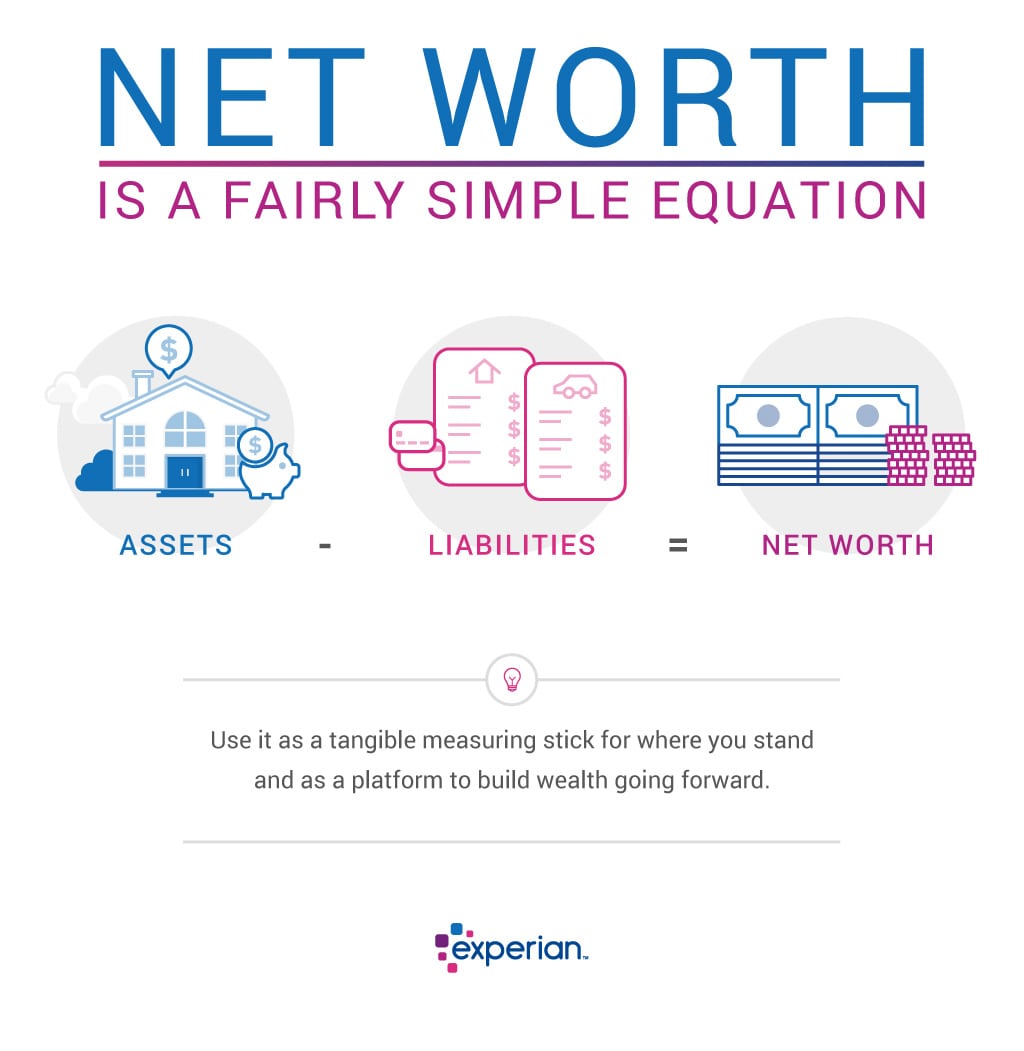

A person's overall financial position is often summarized by a single figure: the difference between total assets and total liabilities. This calculation, representing the net value of an individual's holdings, provides a snapshot of their financial health. Assets include everything owned, such as cash, investments, real estate, and personal property. Liabilities encompass debts like mortgages, loans, and outstanding credit card balances. Subtracting the total liabilities from the total assets yields the figure that represents one's current financial standing.

This figure, this single number, is often crucial for various purposes. It helps in evaluating financial progress, determining borrowing capacity, and making informed investment decisions. Furthermore, the concept allows individuals to track their financial growth over time. The historical context of this concept can be traced back to early financial accounting practices, continually evolving with changes in economic circumstances and investment opportunities. This metric can guide decisions regarding saving, investing, and planning for the future.

| Name | Estimated Net Worth (USD) | Industry/Source of Wealth | Year of Significant Achievement |

|---|---|---|---|

| Elon Musk | ~200 Billion | Technology (SpaceX, Tesla) | 2018 |

| Jeff Bezos | ~150 Billion | E-commerce (Amazon) | 2010 |

| Bill Gates | ~120 Billion | Technology (Microsoft) | 1980s |

The following sections will explore specific aspects of financial well-being, including the use of this single metric to assess an individual's or a business' financial standing, and the potential factors impacting it.

Net Worth

Understanding net worth is crucial for assessing financial health and making informed decisions. This comprehensive overview highlights key facets of this financial metric.

- Assets

- Liabilities

- Valuation

- Financial health

- Investment

- Growth

- Change

- Planning

Net worth, a measure of financial position, is determined by subtracting liabilities from assets. Valuation methods for assets, such as real estate or stocks, fluctuate, influencing net worth changes. Strong financial health often correlates with positive net worth growth, influenced by prudent investment choices. Monitoring these changes over time helps individuals plan for the future. For example, a successful business owner with significant assets and modest debts demonstrates a high net worth, contrasting with an individual with substantial debts and few valuable assets, indicating a negative net worth. This metric guides planning by projecting future financial standings based on anticipated changes.

1. Assets

Assets are the foundation of net worth. Their value, directly impacting the calculation, forms a crucial component. Tangible assets, like real estate and vehicles, and intangible assets, such as intellectual property or stocks, contribute to a positive net worth. Appreciation in asset value leads to a rise in net worth; conversely, asset depreciation or loss diminishes net worth. A portfolio of diverse assets, well-managed and strategically diversified, is often associated with increased net worth stability. For example, a homeowner with a valuable property and well-managed investments typically has a higher net worth than someone with fewer or poorly performing assets.

The crucial role of assets extends beyond their numerical value. Proper asset management encompasses prudent investment strategies, ongoing maintenance, and careful risk assessment. This crucial aspect emphasizes the importance of understanding asset types, their specific value drivers, and market trends to ensure alignment with financial goals. For instance, investing in a dividend-paying stock that consistently generates income contributes positively to net worth, unlike investments that struggle to maintain or increase their value, possibly resulting in a net worth decline. The selection and management of assets are vital factors in building and maintaining financial stability and growth.

In summary, assets are indispensable components of net worth. Understanding asset valuation, types, and management practices is critical for building, maintaining, and ultimately growing net worth. The relationship between assets and net worth is a dynamic one, highlighting the necessity of ongoing evaluation and strategic adjustments to ensure long-term financial health.

2. Liabilities

Liabilities represent financial obligations. They directly impact net worth by reducing the overall value. A higher level of liabilities often results in a lower net worth, indicating a potential financial strain. The nature and size of liabilities significantly influence an individual's or entity's financial standing. For instance, substantial mortgage debt or outstanding loans can substantially reduce net worth, highlighting the importance of managing these obligations.

The relationship between liabilities and net worth is inherently subtractive. For every dollar owed, the net worth diminishes by that amount. This inverse relationship emphasizes the importance of responsible borrowing and debt management. Effective debt management strategies often involve meticulous budgeting, timely repayments, and exploring options to reduce outstanding debts. A borrower diligently managing debt obligations is more likely to demonstrate a positive and stable net worth. Conversely, accumulating substantial debt without appropriate repayment strategies will likely result in a decreased net worth over time. Real-world examples range from individuals with high credit card balances impacting their overall financial well-being to companies burdened with significant outstanding debt potentially leading to financial distress. This directly connects the concept of liabilities to the broader theme of responsible financial planning and decision-making.

In conclusion, liabilities represent a critical component of financial assessments. Understanding their impact on net worth is essential for making informed financial decisions. Responsible debt management, strategic repayment plans, and careful consideration of borrowing limits are crucial for maintaining a healthy net worth. This connection between liabilities and net worth underscores the importance of proactive financial management, crucial for long-term financial stability.

3. Valuation

Valuation is the cornerstone of determining net worth. Accurate valuation of assets underpins the calculation, directly affecting the resulting figure. Changes in asset valuations translate directly into shifts in net worth. For instance, a rise in the market value of a company's stock portfolio results in an increase in the company's net worth, while a decline in property values reduces an individual's net worth. The accuracy and reliability of valuation methods employed are critical to a precise representation of financial standing.

Several methods exist for asset valuation, each with its own complexities and potential sources of error. Real estate appraisal, for example, considers factors like location, condition, comparable sales, and market trends. Stock valuations utilize various models, including discounted cash flow analysis or price-to-earnings ratios, which are susceptible to the uncertainties inherent in future projections. Appropriate valuation methods are critical to avoid misleading financial assessments, whether for personal wealth or business valuation. Incorrect valuation can lead to inaccurate financial planning, unsuitable investment decisions, or even tax liabilities. The significance of consistent and credible valuation methods in a fluctuating economic environment cannot be overstated.

In essence, accurate valuation is indispensable for a valid net worth calculation. The reliable application of appropriate valuation techniques ensures a comprehensive understanding of financial position, guiding decisions regarding investments, borrowing capacity, and overall financial planning. The potential consequences of inadequate or flawed valuation methodsfrom overestimating assets to underestimating liabilitiescan significantly impact the accuracy and utility of net worth assessments. This underscores the critical importance of employing rigorous and appropriate valuation methodologies for any financial evaluation.

4. Financial Health

Financial health, a critical aspect of overall well-being, is intrinsically linked to net worth. A robust financial health profile often correlates with a positive and growing net worth. Conversely, poor financial health frequently results in a declining or stagnating net worth. Understanding this connection provides valuable insights into managing personal finances and achieving long-term financial security.

- Debt Management

Effective debt management is a cornerstone of financial health. Low levels of high-interest debt, coupled with a proactive approach to repayment, are indicative of good financial health. This includes careful budgeting, minimizing unnecessary spending, and prioritizing debt reduction. Examples include individuals with manageable student loan payments or those successfully paying down credit card debt, demonstrating a commitment to responsible financial behavior and the positive implications for net worth. Failure to manage debt can lead to financial distress, negatively impacting net worth and overall financial health.

- Savings and Investing

Consistent saving and strategic investing are integral components of sound financial health. Individuals actively saving for future goals, like retirement or major purchases, and those investing in diversified portfolios, demonstrate a proactive approach to future financial security. A high savings rate combined with disciplined investing typically translates to long-term net worth growth. In contrast, neglecting saving and investment strategies can lead to a slower rate of net worth accumulation, hindering future financial stability. Examples include individuals with robust retirement accounts or those successfully growing investment portfolios over time.

- Cash Flow Management

Efficient management of cash flow, the movement of money into and out of accounts, is crucial to financial health. Maintaining a positive cash flow, meaning income exceeds expenses, supports consistent debt repayment and provides funds for investment. A well-defined budget, tracking expenses meticulously, and effectively managing income streams are crucial for maintaining healthy cash flow, allowing for higher savings and future investments that positively affect net worth. Ineffective cash flow management, leading to insufficient funds for essential expenses or debt payments, often results in financial difficulties, impacting net worth in the long term. Examples include individuals with detailed budget spreadsheets enabling predictable cash flow to cover daily needs, saving goals, and debt obligations.

- Budgeting and Planning

Comprehensive budgeting and financial planning are essential aspects of financial health. Well-defined budgets, outlining income and expenses, provide a roadmap for financial decisions. Planning ahead for future goals and evaluating financial decisions over time allows individuals to make informed choices. Planning for short-term and long-term goals, like buying a home or funding education, positively impacts net worth by prioritizing responsible financial decision-making. Lack of budgeting and planning skills can lead to impulsive spending, debt accumulation, and, subsequently, an undesirable impact on net worth and overall financial well-being. Examples include individuals with detailed, regularly reviewed financial plans guiding spending decisions and investment strategies, and individuals who adjust financial plans based on market fluctuations and personal circumstances.

In summary, the elements of financial healthdebt management, savings and investments, cash flow management, and budgeting and planningare inextricably linked to net worth. A focus on these components directly influences an individual's financial standing and contributes to a positive financial future. Individuals committed to healthy financial practices are more likely to achieve sustained growth in their net worth, ultimately enhancing their financial security.

5. Investment

Investment decisions directly influence net worth. The choices made regarding investments play a pivotal role in shaping long-term financial standing. Strategic investment decisions can lead to substantial increases in net worth over time, while poor choices can result in diminishing returns and negatively impact overall financial health.

- Diversification

Diversifying investment portfolios across various asset classes reduces risk. This strategy spreads investment capital across stocks, bonds, real estate, and other assets. Reduced risk is associated with a more stable net worth over time. For instance, an investment portfolio containing both growth stocks and income-producing bonds demonstrates diversification. This approach reduces reliance on any single asset's performance, mitigating potential losses in specific sectors, and ultimately contributing to a more resilient and stable net worth.

- Return on Investment (ROI)

Maximizing ROI is crucial for increasing net worth. Investments yielding substantial returns above the prevailing market rates tend to contribute positively to overall financial growth. A high-growth company or a well-performing real estate property can deliver positive ROI, consequently increasing net worth. Conversely, underperforming investments may reduce net worth over time. Careful consideration of potential return and risk tolerance is essential.

- Time Horizon

The investment timeframe significantly impacts potential gains and risks. Long-term investments, particularly those aiming for long-term goals like retirement, may involve higher-risk assets potentially generating substantial returns but also carrying a higher degree of uncertainty. Short-term investments often focus on more stable assets with lower potential returns but lower associated risks. Understanding the investor's time horizon is essential in aligning investment strategies to achieve desired long-term goals in net worth accumulation. For example, a young investor planning for retirement in 40 years can afford a larger portion of their investment portfolio to be allocated toward potentially higher-return assets, while a middle-aged investor approaching retirement may favor more conservative investment options.

- Risk Tolerance

Investors should align investment choices with their risk tolerance. High-risk investments, although potentially delivering high returns, may lead to substantial losses in adverse market conditions. Conversely, low-risk investments typically offer more stability but also lower potential returns. Matching investment choices to individual risk tolerance ensures alignment with financial goals and protects against unforeseen market fluctuations, while contributing to a stable and resilient net worth. Individuals should carefully assess their personal risk tolerance and understand the potential risks associated with various investment vehicles before making decisions.

In conclusion, thoughtful investment strategies, encompassing diversification, maximizing returns, considering time horizons, and matching choices with risk tolerance, are integral to building and maintaining a positive net worth. These factors combine to create a strong framework for long-term financial security. By evaluating these aspects, individuals can make informed choices that effectively support their financial goals and ultimately shape their net worth.

6. Growth

Net worth growth represents a critical aspect of financial progress. The extent and consistency of this growth significantly influence an individual's or entity's overall financial health and security. Examining the factors driving net worth appreciation provides insights into strategies for building long-term financial stability.

- Investment Returns

Investment returns form a primary driver of net worth growth. Effective investment strategies, encompassing diversified portfolios and well-researched choices, often yield positive returns, leading to increases in net worth over time. A consistent history of positive investment returns typically reflects sound investment decisions aligned with long-term financial goals. For instance, successful stock market investments or profitable real estate ventures contribute meaningfully to net worth growth.

- Asset Appreciation

Appreciation in asset value directly contributes to net worth growth. Factors like market conditions, inflation, and the inherent characteristics of the asset itself influence the rate of appreciation. The value of property, for example, can increase due to factors such as rising demand or improvements, thus positively influencing net worth. Likewise, increasing value of collectibles, artwork, or other assets positively impacts the net worth figure.

- Debt Reduction

Debt reduction, through consistent repayment and smart borrowing practices, can indirectly contribute to net worth growth. Decreased debt levels free up resources, potentially allowing for increased investment or savings, which can then contribute positively to overall net worth. Managing debt efficiently and strategically can free up resources enabling a positive net worth trajectory.

- Income Growth

Increased income, whether from employment, entrepreneurship, or other sources, frequently translates into higher net worth. A rise in earnings, accompanied by careful expenditure management, can lead to increased savings and investments, stimulating net worth growth. This underscores the connection between income stability and financial prosperity.

In summary, net worth growth stems from a confluence of factors, including consistent investment returns, asset appreciation, debt reduction, and income growth. Understanding these drivers is crucial for developing effective strategies to achieve long-term financial security and prosperity. A meticulous approach to all these aspects enables sustained growth and stability in net worth, ultimately building a strong financial foundation.

7. Change

Fluctuations in net worth are a natural consequence of economic shifts, personal choices, and market forces. Understanding these changes is crucial for effective financial management and long-term planning. The dynamic nature of net worth highlights the importance of ongoing assessment and adaptation to maintain financial stability.

- Market Volatility

Market fluctuations, encompassing stock market swings, interest rate changes, and economic recessions, directly impact asset values. Declines in market value can decrease net worth, while increases can elevate it. For example, a downturn in the stock market might cause a significant reduction in investment portfolios, thereby decreasing overall net worth. Conversely, a period of sustained economic growth often leads to increased asset values and a corresponding rise in net worth.

- Investment Decisions

Strategic investment decisions, including asset allocation choices and the selection of specific investment instruments, play a crucial role in shaping net worth trajectories. Effective diversification and prudent choices contribute to a more resilient net worth, while inappropriate or poorly timed investments can diminish net worth. Examples include investments in companies experiencing sudden downturns or the sale of undervalued assets. These decisions can lead to substantial changes in a person or entity's net worth.

- Financial Obligations

Changes in financial obligations, including debt accumulation, repayments, and loan modifications, directly influence net worth. Increased debt reduces net worth, while debt reduction increases it. The management of financial obligations, including mortgages, loans, and credit card balances, significantly impacts net worth stability over time. For example, taking on substantial new debt to finance a large purchase temporarily lowers net worth; conversely, consistently paying down debt will elevate net worth. Careful planning and disciplined repayment strategies are essential.

- Life Events

Significant life events, such as career changes, marriage, divorce, or the birth of a child, can dramatically alter financial situations and, consequently, net worth. These events may lead to adjustments in income, expenditure patterns, and investment decisions. A career promotion typically leads to increased income, potentially impacting net worth positively. Conversely, unexpected expenses associated with personal life events can reduce net worth if not anticipated and addressed.

In essence, net worth is a dynamic metric reflecting various influences. Understanding these changesdriven by market forces, investment decisions, financial obligations, and life eventsis paramount for effective financial management. Continuous monitoring, evaluation, and adaptation are essential to maintain a stable and positive net worth over time.

8. Planning

Strategic planning is fundamental to achieving and maintaining positive net worth. Effective planning encompasses a proactive approach to financial management, anticipating future needs and opportunities. It serves as a roadmap, guiding decisions and actions that influence the trajectory of financial health and overall wealth. A comprehensive planning framework allows for adjustments to economic conditions, enabling adaptability and ensuring the pursuit of long-term financial well-being.

- Short-Term Financial Planning

Short-term planning focuses on immediate financial goals, such as managing monthly budgets and meeting short-term obligations. Developing a detailed budget, tracking income and expenses, and prioritizing debt repayment are key elements. A well-structured short-term plan ensures adequate funds for essential expenditures while allowing for savings and investment. Real-world examples include creating a monthly budget, outlining expenses, and setting savings targets for upcoming purchases, providing the foundation for future financial security.

- Long-Term Financial Goals

Long-term planning extends beyond immediate needs, considering aspirations for the future, such as retirement, education, or major purchases. Identifying and prioritizing these objectives, coupled with realistic estimations of associated costs, lays the groundwork for consistent saving and investment strategies. This multifaceted approach encompasses retirement planning, establishing emergency funds, and funding future educational needs, providing a clear roadmap for achieving long-term financial goals and bolstering net worth. Examples range from setting up a retirement account to planning for children's college funds, illustrating the importance of long-term foresight.

- Risk Management Strategies

A robust financial plan incorporates risk management strategies, recognizing potential economic downturns or personal circumstances. Contingency planning, encompassing provisions for unforeseen events such as job loss or significant medical expenses, is vital for maintaining financial stability. Planning ahead allows for adapting to market changes or unforeseen circumstances, safeguarding against potential threats to net worth. A comprehensive plan includes having adequate insurance, maintaining emergency funds, or creating backup financial plans in the case of unforeseen life events, illustrating the importance of anticipating and mitigating potential risks.

- Investment Strategies

A comprehensive financial plan often incorporates investment strategies that align with long-term goals and risk tolerance. This includes diversification across asset classes, aligning investments with anticipated needs and future objectives. The plan incorporates diversification, risk tolerance, and expected returns, facilitating informed investment decisions aligned with overall financial goals. This includes developing a portfolio mix tailored to an individual's risk tolerance and anticipated time horizon, optimizing returns while mitigating potential risks, strengthening net worth and securing a stable financial future. Examples include constructing a balanced portfolio that includes stocks, bonds, and other assets, demonstrating the significance of strategic investment in building net worth.

In conclusion, planning forms the bedrock of successful net worth management. By incorporating short-term budgeting, long-term goal setting, risk mitigation, and strategic investment, individuals can create a roadmap for financial security. A well-defined plan allows for adjustments based on life events and market fluctuations, ultimately strengthening the foundation for continued net worth growth and overall financial success. Careful consideration of these facets creates a stable financial future and strengthens the foundation of long-term financial security.

Frequently Asked Questions about Net Worth

This section addresses common inquiries regarding net worth, a crucial measure of financial standing. Clear and concise answers provide a fundamental understanding of the concept.

Question 1: What is net worth, precisely?

Net worth represents the difference between total assets and total liabilities. Assets encompass everything owned, including cash, investments, property, and other holdings. Liabilities represent outstanding debts, such as loans, mortgages, and credit card balances. Subtracting liabilities from assets yields the net worth figure, reflecting an individual's or entity's overall financial position.

Question 2: How is net worth calculated?

Net worth is calculated by summing the value of all assets and subtracting the total value of all liabilities. Precise asset valuations are essential for an accurate net worth calculation. Asset values, like real estate or investments, can fluctuate, leading to variations in the net worth figure over time.

Question 3: Why is understanding net worth important?

Understanding net worth provides a comprehensive view of financial health. It aids in financial planning, evaluating financial progress, assessing borrowing capacity, and making informed investment decisions. Tracking net worth changes over time allows for evaluation of financial strategies and adjustments.

Question 4: What factors influence net worth?

Numerous factors influence net worth, including asset valuation, market fluctuations, debt levels, and income. Changes in asset values, whether increases or decreases, directly impact the net worth calculation. Effective debt management and consistent income are essential components of stable or increasing net worth.

Question 5: How can net worth be improved?

Strategies for improving net worth include increasing assets through prudent investment decisions, reducing liabilities through responsible debt management, and maintaining consistent income. Careful planning and diligent tracking of financial activities are key components in achieving positive net worth growth.

In summary, understanding net worth is a fundamental aspect of personal finance. It provides a crucial metric for assessing financial health, making informed decisions, and pursuing financial goals. Consistent monitoring and proactive management of finances are vital for maintaining and enhancing overall financial well-being.

The following sections will delve deeper into specific aspects of net worth, exploring the intricacies of asset management, debt strategies, and long-term financial planning.

Conclusion

This exploration of net worth reveals a multifaceted concept crucial for financial well-being. The calculation, derived from the difference between total assets and liabilities, provides a snapshot of an individual's or entity's overall financial position. Key factors influencing net worth include asset valuation, market fluctuations, debt management, investment decisions, and income growth. A comprehensive understanding of these elements is essential for informed financial planning and achieving long-term financial security. The dynamic nature of net worth necessitates continuous monitoring and adjustments to adapt to changing economic landscapes and personal circumstances.

Maintaining a healthy net worth is not merely about accumulating wealth; it's about establishing a strong financial foundation for future aspirations. Understanding the principles outlined in this analysis provides a framework for proactive financial management, enabling individuals and entities to navigate economic uncertainties and strive for sustained financial success. The importance of informed decisions and diligent planning cannot be overstated in the pursuit of a positive and growing net worth.

You Might Also Like

Don Henley Daughter's Wedding: A Celebration!Rodney Carrington Net Worth 2024: Latest Figures & Insights

Bing Crosby's Net Worth: A Look At The Legendary Crooner's Fortune

Sean Hannity Fox News Salary: 2023 Earnings Revealed!

Rodney Carrington Net Worth: A Deep Dive Into His Fortune

Article Recommendations

- Unraveling The Financial Success Of Russell Wong A Deep Dive Into His Net Worth

- Unveiling The Enigma The Life And Legacy Of James Bean Thornton

- Unveiling The Life Of 16051575158517401575 16081740170515781608158517401575 16071606157515741608 A Journey Beyond The Shadows